The Union Budget 2025 has introduced significant changes that directly affect Non-Resident Indians (NRIs), particularly in areas of taxation, remittance policies, and financial compliance. While some measures provide relief, others impose additional financial planning requirements. Here’s an in-depth analysis of the key changes and their implications for the global Indian diaspora.

Revised Income Tax Slab Rates for NRIs

The budget has realigned tax slabs to make taxation more progressive. The exemption threshold has increased, providing some relief to middle-income earners. However, the highest tax bracket remains unchanged for individuals earning above ₹24 lakh per annum.

| Income Tax: Slab Rates Old / New | |||||

|---|---|---|---|---|---|

| Annual Income | Old Regime | Annual Income | New Regime FY 2024-25 | Annual Income | Budget 2025 FY 2025-26 |

| < 2.5 Lakhs | Exempt | < 3 Lakhs | Exempt | < 4 Lakhs | Exempt |

| 2.5 – 5 Lakhs | 5% | 3-7 Lakhs | 5% | 4-8 Lakhs | 5% |

| 5 – 10 Lakhs | 20% | 7-10 Lakhs | 10% | 8-12 Lakhs | 10% |

| > 10 Lakhs | 30% | 10-12 Lakhs | 15% | 12-16 Lakhs | 15% |

| 12-15 Lakhs | 20% | 16-20 Lakhs | 20% | ||

| > 15 Lakhs | 30% | 20-24 Lakhs | 25% | ||

| > 24 Lakhs | 30% | ||||

Rebate: Existing Rs 7 Lakhs | Proposed Rs 12 Lakhs (Only for Residents)

The revised structure increases the exemption threshold and lowers tax rates for certain brackets, offering incremental benefits for middle-income NRIs. However, high-income earners above ₹24 lakh will continue to face the highest tax rate of 30%.

Rebate on Tax – No Benefit for NRIs

The government has increased the rebate threshold under Section 87A from ₹7 lakh to ₹12 lakh, but this is available only to resident Indians. NRIs do not qualify for this rebate, emphasizing the need for structured tax planning. NRIs must structure their taxable income efficiently, as they cannot claim the increased rebate benefit.

Surcharge & Cess Adjustments

The surcharge rates on high-income NRIs remain unchanged, but there is a notable relief for ultra-high earners (₹5 Cr+ income).

| Surcharge Table | ||

|---|---|---|

| Income Range (INR) | Surcharge (FY 2024-25) | Surcharge (FY 2025-26) |

| 0 to 50 Lakhs | NIL | NIL |

| 50 Lakhs to 1 Cr | 10% | 10% |

| 1 Cr to 2 Cr | 15% | 15% |

| 2 Cr to 5 Cr | 25% | 25% |

| Above 5 Cr | 37% | 25% |

- Surcharge on Dividend and Capital Gain (Shares/MF) – Maximum 15%

- Education Cess 4%

The biggest relief is for those earning above ₹5 crore, as the surcharge has been reduced from 37% to 25%. Additionally, the maximum surcharge on dividends and capital gains (from shares or mutual funds) has been capped at 15%, benefiting NRIs engaged in equity investments.

Extended Timeline for ITR-U (Updated Return Filing)

ITR U – UPDATED RETURN

3 Years from End of Relevant FY – Now 5 Years

| Timeline | Additional Tax + Interest | Financial Year |

|---|---|---|

| Within 2 Years | 25% | FY 2023-24 |

| 2 Years to 3 Years | 50% | FY 2022-23 |

| 3 Years to 4 Years | 60% | FY 2021-22 |

| 4 Years to 5 Years | 70% | FY 2020-21 |

NRIs now have an extended timeline of 5 years to file updated returns, instead of 3 years previously. However, the penalties for delayed filing have increased:

Additionally, ITR-U cannot be filed if:

- It is a return of loss

- It reduces the tax liability

- It results in a refund

This change helps NRIs correct omissions in tax filings but comes with higher penalties.

TCS under LRS – No Relief for NRIs

Though the Budget has eased Tax Collected at Source (TCS) rules under the Liberalised Remittance Scheme (LRS) for residents, no such benefit extends to NRIs. The TCS remains at 20% for remittances exceeding ₹10 lakh, except for education and medical treatment.

| TCS under LRS (For Residents Only) | ||

|---|---|---|

| Type of Remittance | Present Rate & Threshold | Proposed Rate & Threshold |

| Education: Amount taken as Loan from Financial Institution | 0.5% in excess of Rs 7 Lakhs | NIL |

| Education: Amount not taken as Loan | 5% in excess of Rs 7 Lakhs | 5% in excess of Rs 10 Lakhs |

| Medical Treatment | 5% in excess of Rs 7 Lakhs | 5% in excess of Rs 10 Lakhs |

| Any Other Case | 20% in excess of Rs 7 Lakhs | 20% in excess of Rs 10 Lakhs |

While residents benefit from relaxed LRS rules, NRIs remitting funds under non-education or non-medical categories continue to face the 20% TCS burden.

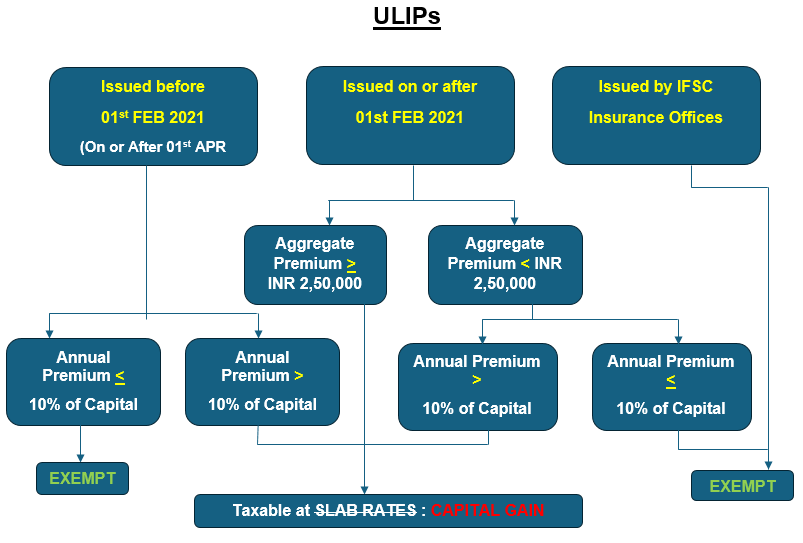

Changes in ULIP and Life Insurance Taxation

Redemption of ULIPs

Taxation on ULIPs (Unit-Linked Insurance Plans)

- Before Feb 1, 2021: Premiums <10% of sum assured → Exempt

- After Feb 1, 2021: If annual premium exceeds ₹2.5 Lakh, maturity proceeds are taxable as capital gains (12.5%)

- IFSC-issued ULIPs remain tax-free

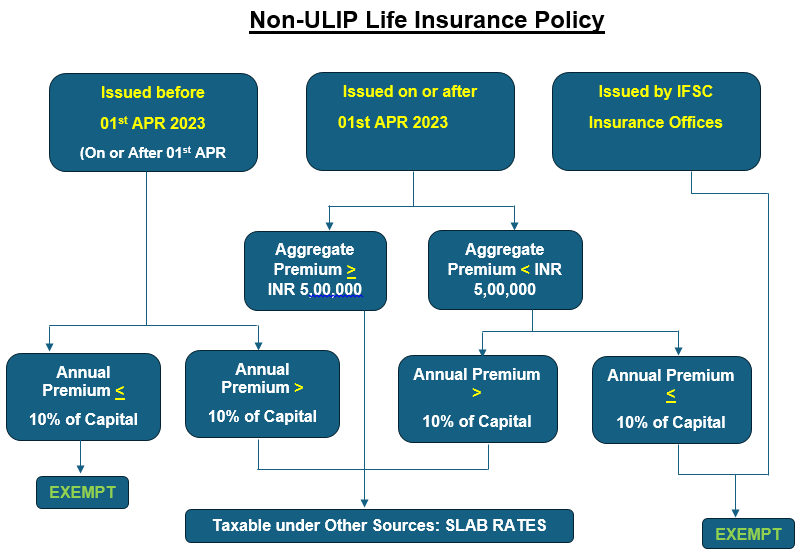

Life Insurance Policy (Non ULIP)

Taxation on Non-ULIP Life Insurance

- Before Apr 1, 2023: Premiums <10% of sum assured → Exempt

- After Apr 1, 2023: If aggregate premium > ₹5 Lakh, proceeds taxable as ‘Income from Other Sources’ at slab rates

This change affects NRIs investing in high-premium life insurance policies as a tax-free investment avenue.

What Should NRIs Do?

While the Budget 2025 has introduced minor relief measures, NRIs still face challenges in taxation, remittances, and compliance. Here’s how NRIs should adapt:

✔ Tax Planning: Use exemptions wisely and plan income structuring to avoid high surcharge brackets.

✔ ITR Compliance: Utilize the extended ITR-U period but avoid situations leading to penalties.

✔ Investment Strategy: Consider re-evaluating insurance and investment decisions in light of new taxation.

✔ Remittance Planning: Factor in TCS implications while making cross-border transactions.

For NRIs earning over ₹5 crore, the reduced surcharge is a welcome move, but the lack of rebate benefits and continued TCS obligations remain key concerns. As tax laws evolve, proactive financial planning is essential for maximizing benefits and minimizing liabilities.